How much should you really save?

Deriving the saving rate that keeps your lifestyle constant over time

Ask ten people in finance how much you should save for retirement and you’ll get ten confident but different answers.

Some will tell you that 20% of your income is a solid benchmark. Others insist that you should save as aggressively as possible while you are young. In more online corners of the finance world, the answer is often framed as an identity rather than a calculation: FIRE or nothing1.

What is striking is not that these answers differ, but that almost none of them explain why a particular saving rate should be appropriate in the first place. They tend to rely on convention, repetition, or ideology rather than on a clearly articulated economic argument.

So let’s approach the question from a different angle.

Imagine you could design your financial life from scratch. No rules of thumb, no community norms, no moral language about discipline or restraint. Just your preferences and some basic arithmetic.

What would you actually want your life to look like?

Most people, when pressed, do not say that they want to live frugally for decades so that their future self can finally enjoy a higher standard of living. But they also rarely say that they want to consume as much as possible today and deal with old age later.

What they usually describe is something far more modest — and at the same time much harder to formalize: they want their life to feel broadly similar over time.

They want roughly the same quality of housing, the same freedom to travel, and the same sense of financial ease throughout their adult life. In short, they are not aiming to become progressively richer or poorer over time — they are aiming for stability.

Why this clashes with FIRE (and most finance advice)

This perspective also explains why the consumption smoothing framework sits somewhat uneasily with large parts of modern personal finance culture.

FIRE strategies, in particular, are built around a deliberate imbalance. They assume significantly lower consumption early in life in order to buy freedom later on. That can be a perfectly rational choice, but it is explicitly a choice to accept uneven consumption over time.

Consumption smoothing rejects that premise. It asks a colder and more uncomfortable question: What is the highest lifestyle I can afford if I refuse to let my standard of living jump around over time?

There is no sprint phase in this model and no promise of early escape. Instead, it assumes continuity. You choose a lifestyle and insist on financing that same lifestyle both while working and in retirement.

What this article actually does

The goal of this article is deliberately narrow and analytical. The aim is to derive a closed-form formula for the saving rate that allows an individual to keep real consumption constant over their entire lifetime. The purpose is not precision forecasting. It is to understand structure — to see where saving rates actually come from once you stop relying on heuristics.

We start with a frictionless world and then introduce two unavoidable real-world frictions. The first is inflation, which turns nominal returns into real purchasing power. The second is taxation of retirement withdrawals, which permanently raises the cost of future consumption.

At the same time, it is important to be explicit about what this framework does not capture. It does not model sequence-of-return risk, return volatility, behavioral responses, or uncertain life expectancy. For that reason, the saving rates derived here could be interpreted as a floor, not as a safety margin.

If you’re primarily interested in the result and want to skip the mathematical derivation, you can find a simple online calculator that implements the framework discussed here. The rest of this article focuses on the intuition and structure behind it.

Step 1: The frictionless core

Let’s say your current income (G) is either used for consumption (C) or saving (S). We could denote this as

Another way of expressing this is by using a percentage savings rate (R), which will simplify some calculations later on. With some re-arranging we can say that the consumption while working equals your income times 1 less your savings rate:

, which is the same as saying your savings rate equals

Wealth at retirement consists of accumulated savings plus initial wealth (V_0). Hence, if you save for T years at an annual return of i your future wealth will be:

If you then withdraw at a post-retirement return j for retirement duration M, your annual withdrawal W satisfies:

Since we want our withdrawals during retirement to be the same as our consumption while working we can re-arrange the above to:

Solving for the optimal savings rate (R) leads us to:

This equation is the mathematical core of consumption smoothing and already illustrates an important point: saving rates are not arbitrary. They are the result of time, returns, and desired consumption paths interacting with one another.

And yes, this formula is a bit of a beast. It’s not intuitive, it’s not elegant, and it’s certainly not something you’d want to memorize. But it is mathematically honest - and that turns out to be more useful than beauty in this context.

Step 2: Reflecting key frictions (inflation and taxes)

In reality, nominal returns are irrelevant for consumption decisions. What matters is purchasing power, after accounting for inflation (π). We therefore work with real returns, defined as:

In addition, we assume that retirement withdrawals are taxed at a flat rate τ and that this tax applies to the full withdrawal amount, not just to gains.

Under these assumptions, the saving rate that keeps net consumption constant over time becomes:

This is the central result of the framework.

It represents the theoretically ideal and mathematically correct saving rate implied by the assumption of perfectly smoothed real consumption, given returns, inflation, taxation, time horizons, and starting wealth.

Importantly, this saving rate is not a recommendation in a practical sense. It is a benchmark. It tells you what the arithmetic demands if you insist on constant consumption and if the world behaves exactly as assumed. Real-world uncertainty - particularly sequence-of-return risk and longevity risk - will typically require saving more than this formula suggests, not less.

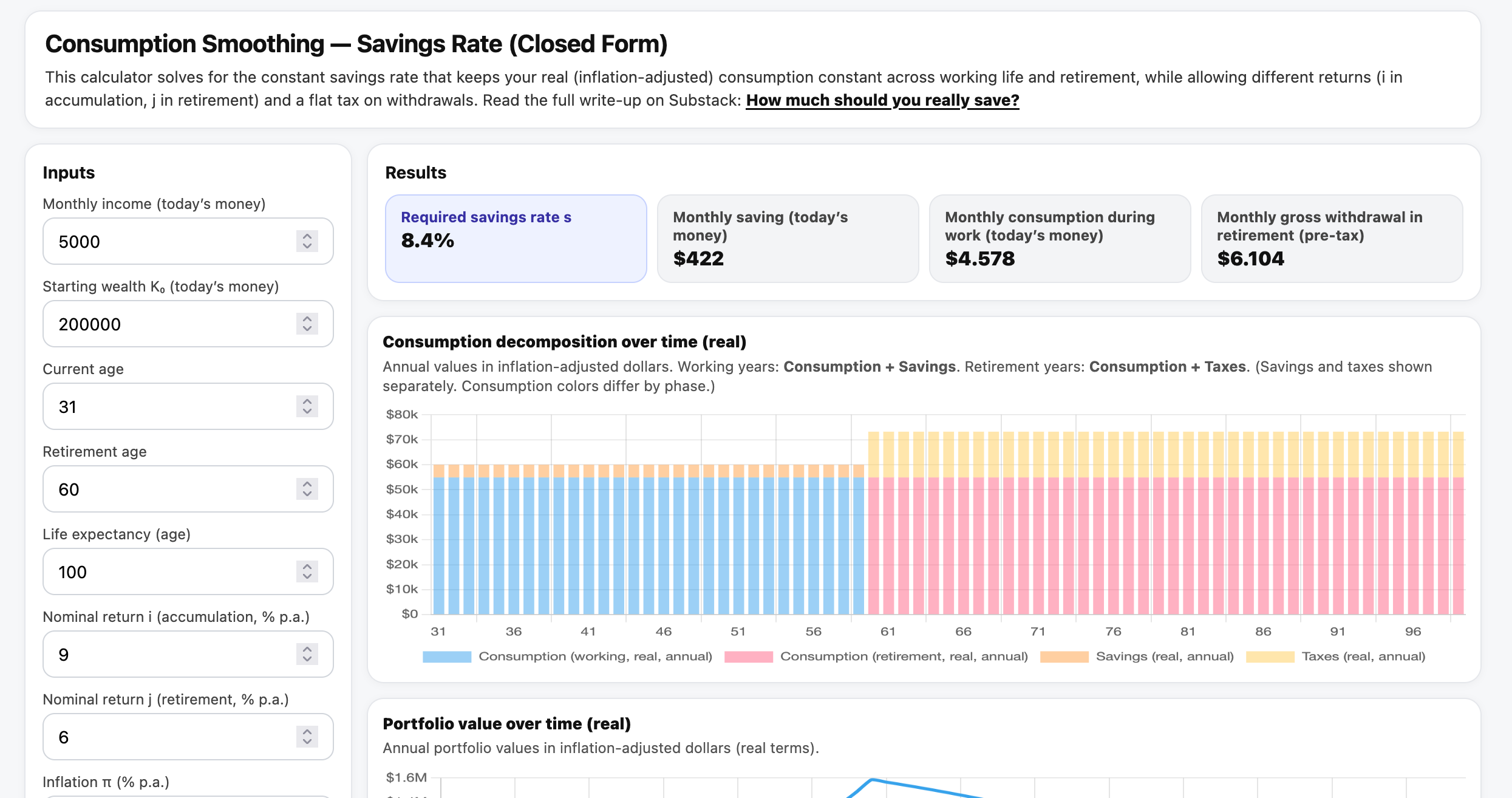

Applying the framework: an interactive calculator

To make the framework usable without copying formulas into a spreadsheet, I’ve built a simple online calculator that implements the exact model described above:

https://seekingalpha1.github.io/savingsrate-calculator/calculator.html

Beyond the headline savings rate, the calculator also visualizes what the model implies over time. It shows how annual consumption, savings, and taxes evolve across age, and how the real portfolio value develops through accumulation and decumulation.

The calculator does not add new assumptions. It is simply a transparent implementation of the closed-form solution derived above. As discussed, the resulting savings rate should therefore be interpreted as a theoretical benchmark rather than a safety margin, especially since the model abstracts from return volatility and sequence-of-returns risk.

Summary

Seen through the lens of consumption smoothing, saving is neither discipline nor deprivation. It is simply the act of pre-paying future consumption at market prices, under inflation and taxation.

Once you think about saving this way, the question “How much should I save?” stops being philosophical. It becomes what it always should have been: an engineering problem under uncertainty.

And for that, the presented closed-form equation above is a surprisingly good place to start.

In a follow-up article, I’ll take a closer look at one of the most important limitations of the framework above: sequence-of-returns risk. While the model assumes smooth, deterministic returns, real portfolios experience volatility, and the timing of returns can materially affect sustainable consumption. Understanding how this risk interacts with consumption smoothing helps explain why practical saving rates often need to sit above the theoretical benchmark derived here.

For readers who want to apply this framework directly to their own situation, I’ve made a simple online calculator available here: https://seekingalpha1.github.io/savingsrate-calculator/calculator.html

It implements the closed-form consumption smoothing model from this article, including inflation, different pre- and post-retirement returns, starting wealth, and a flat tax on retirement withdrawals.

FIRE (“Financial Independence, Retire Early”) refers to a family of strategies that aim to maximize saving rates early in life in order to reach financial independence and exit paid work well before traditional retirement age. The approach typically implies deliberately uneven consumption over time.